Your first BAS statement is always the one that gets you. You’re registered for GST, the quarter ends, and suddenly there’s a form sitting in the ATO portal with labels like G1, 1A, W2, T7. None of which made sense when you registered the business.

A BAS statement (formally called a Business Activity Statement) is the form Australian businesses use to report and pay GST, PAYG withholding, and PAYG instalments to the ATO. If your business is registered for GST, you’re required to lodge one: quarterly for most, monthly for larger operators, annually for a small group.

The form itself isn’t the hard part. The hard part is getting your figures right before you hit submit, because the ATO treats BAS errors as seriously as income tax errors. Under-reporting GST by $3,000 on one quarter’s BAS looks different to the ATO than the same mistake on your annual tax return.

This guide walks through what goes on each label, when your BAS is due, how to lodge it, and the seven mistakes that trip up most business owners. It’s written from the perspective of a registered BAS agent, so where the ATO’s guidance gets vague, I’ll tell you what actually happens in practice.

What is a BAS statement?

Think of a BAS as a periodic statement of what your business has collected, withheld, and owes during a reporting period. It doesn’t replace your annual tax return. The two are separate lodgements that feed into each other.

Most BAS statements report three things. GST on sales you’ve made and purchases you’ve paid. PAYG withholding tax you’ve deducted from employee wages. PAYG instalments toward your own business income tax. Larger businesses may also report FBT instalments, fuel tax credits, or wine equalisation tax, but those apply to a small minority.

The BAS exists because the ATO wants tax money to flow in periodically, not once a year at tax time. If you’re GST-registered, you’re effectively acting as a tax collector on the ATO’s behalf – collecting GST from customers, deducting tax from wages, and paying it through the BAS.

Your BAS doesn’t calculate your business’s income tax. That happens in the annual tax return. The BAS handles indirect taxes (GST) and prepayments (PAYG instalments).

Who needs to lodge a BAS?

You need to lodge a BAS if your business is registered for GST. That’s the single test — not your turnover, not your entity type, not whether you have employees.

GST registration is compulsory once your turnover hits $75,000 (or $150,000 for non-profits). Ride-share drivers and taxi operators are required to register regardless of turnover. Below $75,000 you can register voluntarily (see the ATO GST registration guide), and some businesses do, usually because their customers are also GST-registered and expect tax invoices.

Your reporting frequency depends on your GST turnover:

| GST turnover | Reporting frequency |

|---|---|

| Under $20 million | Quarterly (most small businesses) |

| $20 million or more | Monthly (compulsory) |

| Under $75,000 voluntarily registered | Annually (optional) |

A quick reality check: if you’re registered for GST but had no activity in a reporting period, you still have to lodge a nil BAS. Skipping it, even for a dead quarter, triggers the same late lodgement penalty as a missed active one.

How do I prepare to lodge my BAS?

Accurate BAS starts long before you open the lodgement portal. By the time the quarter ends, either your records are in order or they’re not. Sorting out three months of receipts in the 28 days after quarter end is where most mistakes happen.

Here’s what needs to be reconciled before you start the BAS:

- Sales records. Every invoice issued in the quarter, split between taxable sales, GST-free sales, and input-taxed sales. Most accounting software does this automatically if the tax codes are set correctly.

- Expense receipts. Every purchase with a valid tax invoice if you’re claiming GST credits. Anything over $82.50 (incl. GST) must have a valid tax invoice with the supplier’s ABN.

- Payroll records. Gross wages paid (W1) and tax withheld (W2) for the period. Your payroll software should match your BAS figures exactly.

- Bank reconciliation. The number one BAS mistake is lodging without reconciling the bank first. If the bank statement doesn’t match your accounting software, your BAS numbers are wrong.

One missing bank transaction won’t blow up your BAS, but a month of unreconciled entries can shift your GST position by thousands.

A solid bookkeeping process makes BAS a 15-minute job. Without it, you’re doing forensic accounting every three months.

How do I calculate the numbers on my BAS?

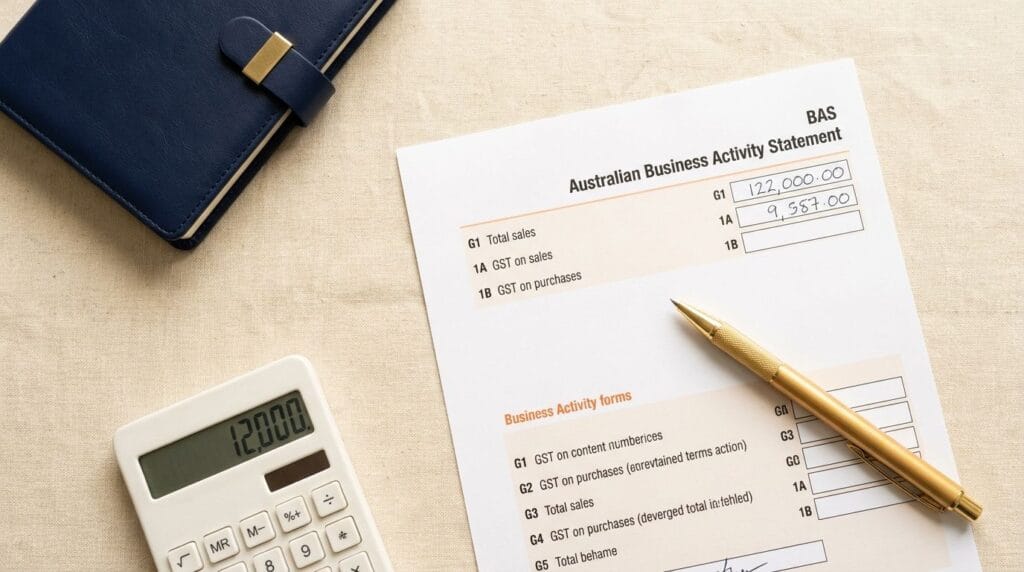

The ATO form uses label codes that sound technical but map to straightforward calculations.

GST on sales (label 1A)

Add up all taxable sales for the period (label G1). GST on sales is then G1 ÷ 11. The divide-by-11 rule works because GST is 10% of the pre-GST price, which is 1/11 of the GST-inclusive total.

Worked example. Total taxable sales for Q2: $132,000 (GST-inclusive). GST on sales = $132,000 ÷ 11 = $12,000 at label 1A.

GST on purchases (label 1B)

Same principle, in reverse. Add all creditable purchases (those with valid tax invoices, for business use). GST on purchases = Total purchases ÷ 11.

Worked example. Total creditable purchases for Q2: $66,000 (GST-inclusive). GST on purchases = $66,000 ÷ 11 = $6,000 at label 1B.

Net GST payable = $12,000 − $6,000 = $6,000 owing to the ATO.

The divide-by-11 rule only works on GST-inclusive totals. If your accounting software shows GST-exclusive figures, the calculation is different.

PAYG withholding (labels W1 and W2)

W1 is total gross wages paid in the period. W2 is total tax withheld from those wages. Both come directly from your payroll system. If they don’t match your payroll reports exactly, something’s wrong.

Worked example. Gross wages paid: $50,000. Tax withheld: $9,500. Report W1 = $50,000 and W2 = $9,500.

PAYG instalment (label T7)

If you’re a PAYG instalment payer, the ATO pre-fills an instalment amount at T7 based on your last tax return. You can either accept it or vary it at T8 if you believe your income will be materially different this year.

Varying T7 downward below a safe threshold exposes you to a general interest charge on the underpayment. Only vary if you have clear evidence your income has dropped.

Stuck on your GST reconciliation?

A registered BAS agent can review your figures before you lodge, catch the common errors, and submit on your behalf. You also get a built-in lodgement extension at no extra cost.

How do I lodge and pay my BAS?

Most business owners have three options for lodging a BAS.

Through your accounting software. Xero, MYOB, and QuickBooks all lodge directly to the ATO via their integrated portals. This is the fastest method once set up. The figures flow straight from your ledger to the form, and you get immediate confirmation.

Through the ATO Online Services for Business portal. If you’re not using integrated software, you can lodge manually through the ATO portal using myGovID. Same form, same due date, more manual data entry.

Through a registered BAS or tax agent. If your lodgement goes through a registered agent, you get the concessional due date, usually around 4 extra weeks for quarterly lodgements. The agent lodges via their practice software.

Paper BAS forms still exist but the ATO has been phasing them out. Unless you have no internet access, don’t use them. (Yes, they really still mail paper forms to some businesses.)

For payment: BPAY with the PRN (payment reference number) from your BAS is the standard. Credit card works but attracts a small surcharge. The payment due date is the same as the lodgement due date. Late payment attracts the general interest charge, which compounds daily at roughly 11% per annum.

When is my BAS due?

Quarterly BAS is due 28 days after the end of each quarter. Monthly BAS is due on the 21st of the following month. Annual BAS follows the same deadline as the annual income tax return, which is 28 February after the financial year end for most businesses.

Lodging through a registered BAS or tax agent gets you roughly 4 extra weeks for most quarterly lodgements, except Q2 (October–December). Q2 already has a longer ATO concession built in for the Christmas period. If a due date falls on a weekend or public holiday, it rolls to the next business day.

For the full quarterly and monthly schedule including weekend adjustments and registered agent extensions, see the ATO’s BAS due dates page.

What are the most common BAS mistakes?

After seven years of reviewing BAS figures, the same mistakes come up again and again. None of them are exotic, but they all cost real money.

1. Claiming GST on expenses without a valid tax invoice. No tax invoice, no GST credit. The ATO can disallow the credit and backdate a penalty. For anything over $82.50 (including GST), hold the invoice.

2. Claiming GST on GST-free or input-taxed purchases. Residential rent, bank fees, and most insurance are input-taxed. No GST on them, nothing to claim. Fresh food, medical services, and exports are GST-free. Running these through as standard GST is one of the most frequent errors.

3. Not reconciling the bank before lodging. If Xero’s bank feed doesn’t match the actual bank balance, your sales and expense totals are off. Every number on the BAS flows from those totals.

4. Misclassifying GST on wages. Employee wages don’t carry GST. Contractor payments usually do (if the contractor is registered). Getting this wrong inflates your GST credits.

5. Reporting PAYG withholding that doesn’t match payroll records. W1 and W2 on the BAS must match the totals in your payroll system exactly. If they don’t, the ATO will reconcile them against STP reporting and flag the variance.

6. Forgetting to lodge a nil BAS. No activity in a quarter still requires a nil BAS. Skipping it triggers the same late penalty as a missed active BAS, at $330 per 28-day period.

The ATO doesn’t distinguish between a forgotten nil BAS and a deliberately missed active one. The penalty is identical.

7. Lodging without reviewing the numbers. The form will let you submit obviously wrong figures. A few quick sanity checks before hitting lodge: Does GST collected look proportional to revenue? Does W2 match your payroll reports? Does the refund or payment amount look right for the quarter?

Mistake #7 is the one that matters most. Most of the others can be caught in five minutes of review.

Here’s what these mistakes actually look like in practice. Last August, a landscaping business owner named Tom came to us after lodging three quarters of BAS himself. He’d been claiming GST credits on his public liability insurance (mistake #2) and hadn’t reconciled his bank account since April (mistake #3). Between the two, his GST position was overstated by $4,800. We corrected the errors on his next BAS using the ATO’s $10,000 voluntary disclosure threshold, but if the ATO had picked it up first, he’d have been looking at a shortfall penalty on top of the interest charge.

When should I use a registered BAS agent?

A registered BAS agent is useful in three specific situations, and optional in most others.

If your GST is complex. Mixed GST-free and taxable sales, import/export activity, the margin scheme for property, or FBT instalments. These are where DIY BAS goes wrong most often. The ATO audits these areas specifically.

If you want the lodgement extension. Registered agents get a 4-week extension on most quarterly lodgements (not Q2). For a business that regularly cuts BAS timing fine, this buys breathing room. (Spoiler: most of our clients signed up because of this, not because they couldn’t do the maths.)

If you want someone to liaise with the ATO on your behalf. Agents can respond to ATO queries, request payment plans, and handle compliance correspondence so you don’t have to be on the phone. For business owners who’d rather not deal with the ATO directly, this is the main reason to use one.

The Tax Practitioners Board register lists every registered BAS and tax agent in Australia. Check before engaging one. Hopkan Partners is a registered BAS agent in Sydney.

You don’t need an agent if your BAS is genuinely simple: single entity, GST-taxable sales only, no employees, software-based bookkeeping. In that case, 30 minutes a quarter is probably enough.

Spending too much time on BAS each quarter?

Hopkan Partners is a Sydney CPA practice and registered BAS agent. We handle BAS preparation and lodgement for Australian businesses. Fixed monthly fee, no surprises. Book a free 30-minute review and we’ll tell you whether your BAS process is working, or where it’s costing you.